Worried about protecting your family’s finances now that you’re in your 30s? Nearly half of UK adults don’t have enough life insurance to cover debts and family costs.

We’ll explain the best life insurance for over 30, its costs, and how to choose wisely. Read on to find affordable options that suit you.

- Protect your future self and those you care about. Even if you don’t have dependents, life insurance can cover debts or help your loved ones handle costs, leaving no one with unexpected burdens.

- Secure lower rates now while you’re young and healthy, no matter what tomorrow might bring.

Life Insurance For People In Their Thirties. Compare Plans From Leading UK Insurers Today

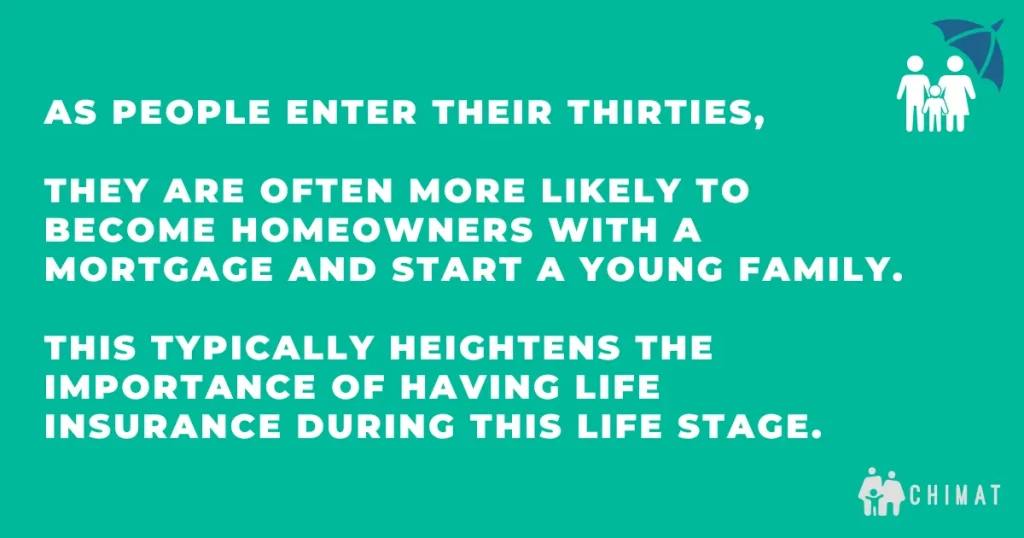

Why Think About Life Insurance in Your 30s?

So, should you get life insurance in your 30s? Life changes fast in your 30s. In our opinion it’s the right time to think about life cover. You’re building your future now, so don’t leave protection out of the picture.

Financial responsibilities

People in their 30s often carry significant financial duties, like mortgage payments or rent. For example, the average UK mortgage is around £1,473 per month and monthly rent averages about £1,223.

- With these daily costs eating up your wages—plus childcare fees averaging £302.10 each week—there’s little room for sudden financial shocks.

- Having children adds more money worries, too. On average, it costs around £166,000 to raise a child to age 18 in the UK.

I can speak from my own first-hand experience: after buying our home and starting a family at 32, guaranteed life insurance over 30 was a key relief against financial stress.

Selecting the right life insurance for people over 30 helps safeguard you from unexpected events that could threaten your family’s finances down the road.

Protecting your family

Taking out life insurance in your 30s helps safeguard your family’s future. Nearly half of UK adults lack life cover or have insufficient protection, leaving loved ones at financial risk.

Average monthly living costs for a family in the UK are £2,700—that’s around £33,000 each year to maintain daily needs like housing, food and bills.

Getting over 30 life insurance offers peace of mind; it ensures that partners and children won’t struggle if the main earner dies suddenly.

Life insurance isn’t for you—it’s for those who depend on you.

Future planning

Life insurance in your 30s lets you plan ahead with peace of mind. From experience, thinking about money for later life doesn’t feel urgent now—but future costs can quickly pile up.

In the UK today, funerals cost around £4,141 on average, and dying overall adds up to roughly £9,658.

On top of that debt—think credit card balances averaging £1,324 and unsecured loans reaching about £4,287—is often left behind for loved ones to handle.

Sorting out a suitable policy such as over 30 guaranteed life insurance or specific plans like life insurance for women over 30 helps meet your family’s future needs.

You clearly set aside funds to pay outstanding debts and protect those who depend on you if you’re no longer around.

It’s smart financial planning. Life insurance in your 30s keeps tomorrow secure while you live fully today.

Try Our Life Insurance Policy Suggestion Tool Below:

Types of Life Insurance for Over 30s

Life insurance isn’t one-size-fits-all; different options fit different needs. Knowing what each policy offers helps you pick what’s right for your life stage in your 30s.

Term life insurance

Term life insurance gives you cover for a set number of years, like 10, 20 or even 30.

For example, a healthy non-smoker aged 30 in the UK can get £124,000 of protection over twenty years for around just £5 per month—or up to £300,000 for about £10 per month.

I took out term life insurance in my early thirties, and it was reassuring and affordable—especially given rising family costs and mortgages at this age.

Term insurance is affordable peace of mind—it helps safeguard your family’s financial future without breaking the bank.

Now, let’s explore another option—decreasing term life insurance.

Decreasing Term life insurance

Decreasing term life insurance offers cover that shrinks in value over the years. This policy is often cheaper than standard term life insurance, making it attractive to people with mortgages or debts that reduce each year.

- For example, a 30-year-old can find decreasing cover of £200,000 for about £6.85 per month over 20 years.

- At age 39, this same cover would cost around £8.71 each month. It suits those who want peace of mind without high costs and is suitable if your needs lessen as time goes on—like paying down your home loan.

Comparing life insurance quotes over 30 can help you see if this option works best for you while managing finances wisely into the future.

Whole of life insurance

Whole of life insurance gives lifelong coverage, as long as you pay your premiums. Unlike term policies that last for a set amount of time—say 20 or 30 years—whole policies won’t expire.

Click To Compare QuotesThis means your loved ones are protected no matter how old you get. However, this type often has higher premiums than term cover because it guarantees a payout whenever death happens.

If you’re thinking about life insurance UK over 30, whole of life cover can secure lasting peace of mind for you and your family. However, make sure the cost fits comfortably into your budget if choosing this route.

Joint life insurance policies

Joint life insurance policies cover two people, often couples or partners. A joint policy pays out just once during the agreed term—usually to the surviving partner.

- For example, at age 30 in the UK, a £150,000 joint policy over 20 years costs around £10.72 each month;

- Buying two single plans instead would cost about £11.44 combined per month.

From personal experience in my early 30s, this small saving can add up over time and makes it easier to manage household budgets together.

Price isn’t everything, though. A joint life plan stops after one payout, even if both partners pass away separately later on.

You must weigh this against your own family situation and decide carefully whether you should get life insurance in your 30s as a couple or choose individual coverage instead for greater flexibility of protection.

How Much Does Life Insurance Cost For A 30 Year Old?

Life insurance costs for a healthy non-smoker aged 30 in the UK start from around £5 per month.

For example, Aviva offers £150,000 of level term cover over 20 years at about £5.76 monthly.

| Provider | Policy Details | Monthly Cost |

|---|---|---|

| Aviva | £150,000 level term cover, 20 years | £5.76 |

| Legal & General | £150,000 level term cover, 20 years | £6.75 |

| Scottish Widows | £150,000 level term cover, 20 years | £6.81 |

| Average (Level) | £200,000 level term cover, 20 years | £6.84 |

| Average (Decreasing) | £200,000 decreasing term cover, 20 years | £5.57 |

Other insurers like Legal & General charge roughly £6.75, and Scottish Widows is slightly higher at £6.81 for the same policy type and length.

Monthly premiums also depend on how much protection you choose and the policy style you prefer—level or decreasing term cover.

A level term life insurance policy offering a payout of £200,000 over 20 years typically costs about £6.85 per month if you’re aged 30; decreasing term cover drops to around £5.56 each month because payouts shrink over time as your debts decrease too.

Understanding what affects your premium helps ensure you get great life coverage at an affordable cost.

Factors Affecting the Cost of Life Insurance in Your 30s

Life insurance costs in your 30s vary widely based on personal factors and choices. Knowing what can affect the price helps you get better cover at a fair rate.

Age and health

In your 30s, age and health greatly affect the cost of life insurance. I took out a policy at age 31, and my premium was lower than that of my older friend, who applied in his early 40s. Premiums rise with age because insurers see more risk as you get older.

Health is key, too. People in good shape enjoy better rates on their policies. My cousin Sarah, for example, is active and healthy; she got an affordable monthly rate easily approved by her insurer last year.

Staying fit matters since insurers favour younger applicants who look after their health, so applying sooner rather than later helps secure lower premiums.

Lifestyle habits

Healthy lifestyle habits greatly affect life insurance costs in your 30s. Smoking heavily impacts these premiums, often raising them by 25%-40% compared with non-smokers.

Drinking large amounts of alcohol, taking part in risky sports or having poor eating habits can also push prices up.

Good choices like regular exercise and balanced meals help show insurers you’re a low-risk client who cares for your health. Insurers tend to reward those who take care of themselves with lower premiums, meaning extra savings each year.

Beyond lifestyle, smoking status is another vital factor that decides how much you pay for your cover.

Smoking status

Smokers in their 30s often pay more for life insurance compared to non-smokers. Insurers see smokers as higher risk due to serious health effects, like heart disease and cancer. Some insurers need you to quit smoking fully for at least one year before giving cheaper rates.

Click To Compare QuotesBeing smoke-free can cut your premiums significantly, saving hundreds of pounds each year on life cover costs. However, even if you currently smoke, numerous affordable policies are available.

Your weight

Smoking isn’t the only lifestyle habit that can affect your life insurance cost. Your weight is important too. Insurance companies look at your body mass index (BMI) to see if you’re within a healthy range.

A higher BMI can signal health risks like heart disease or diabetes, raising your premiums.

- Many companies charge lower rates for those with a BMI between 18.5 and 24.9, as this range shows that people with this weight are less likely to face serious health issues linked to extra weight.

- Being outside this healthy band may lead insurers to put you in a higher risk group, meaning you’ll pay more each month on your policy.

Keeping active and maintaining a balanced diet will help keep both your BMI and premiums down, saving money while looking after yourself in your 30s and beyond.

Occupation

Your weight plays a big role in setting your life insurance costs, but your job matters, too. Some jobs carry more risks than others, like firefighters, police officers, or construction workers, which may cause insurers to charge higher premiums.

I once worked with a friend who was an oil rig diver. At age 32, his monthly premium was nearly double mine because of the danger involved.

Office-based roles like accountants, teachers and IT specialists usually have lower rates. Insurers look closely at what you do every day to set your price.

For instance, if you regularly travel or work at heights, you’ll likely pay extra for cover due to higher risk factors linked to these activities.

Medical history

Family medical history can impact your life insurance cost. Insurers look at conditions like heart disease, diabetes or cancer in parents and siblings.

For example, my friend James saw higher premiums because his dad had early-onset heart problems—though James himself was healthy at 33.

Being open about family health issues is key when applying for cover in the UK. Hiding details can lead to rejected claims later on. Sharing accurate medical facts from your family’s past helps providers set fair prices and keeps you protected.

Next, let’s find out how policy types and coverage amounts affect costs….

Policy type and coverage amount

The type of policy and coverage you pick affects how much you’ll pay each month. Term life insurance is often cheaper, with a fixed coverage length—usually 20 to 30 years—and a set amount paid if you pass away within the term.

One of our clients, Claire, at age 32, chose term life cover worth £150,000 over 25 years. This was enough to cover her mortgage debt, which averages around £127,140 in the UK and provide for her childcare needs.

Whole-of-life policies offer lifetime protection but usually cost more each month since they guarantee a payout.

Decreasing term policies may suit those paying off mortgages. As the outstanding balance drops, so does your coverage and premium cost.

Joint life insurance could appeal as it pays out upon one partner’s death—but keep in mind that it only pays once.

Picking the right policy means thinking clearly about your financial obligations and future goals, which we’ll discuss next.

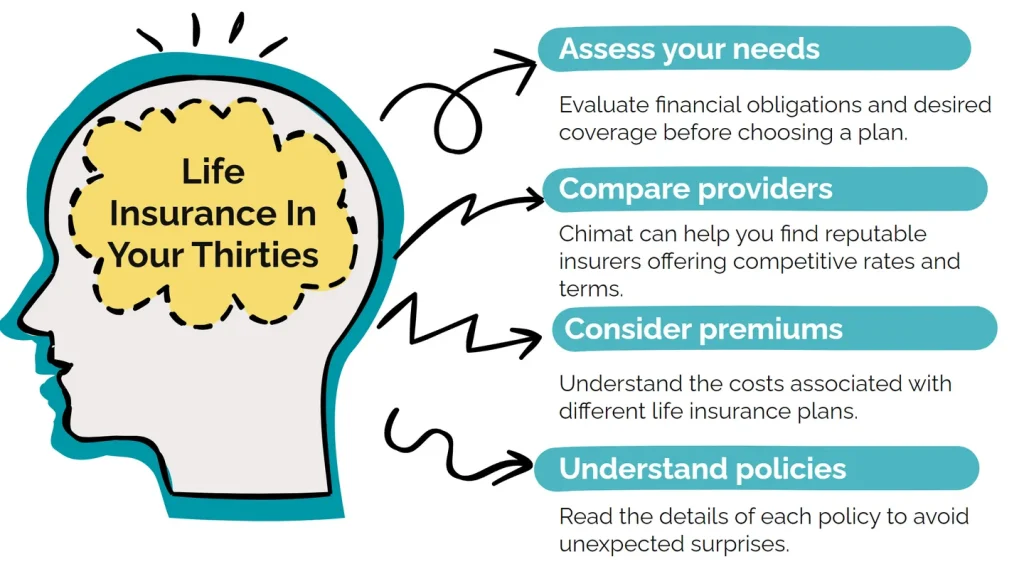

How to Determine the Right Life Insurance Coverage

Finding the right life insurance cover starts with a clear look at your finances today and how they’d change if you were gone.

Think carefully about the costs your family might face, monitor rising prices, and plan ahead for their future security.

Assess your financial obligations

In my early 30s, I faced plenty of new financial obligations. Mortgage payments became my biggest monthly expense at around £1,100 each month for a modest flat in London.

Within two years, childcare fees added another £850 to the budget each month.

On top of these costs are general family living expenses like food bills, petrol and council tax.

Life insurance coverage must reflect these regular outgoings clearly and sensibly. Taking note of what you owe helps identify how much cover your loved ones might need if you’re no longer able to provide income due to illness or death.

This step was crucial when choosing the right policy amount. I made sure it covered at least ten times our yearly household costs for peace of mind.

Plan for future goals

Once you’ve worked out what you owe now, think ahead to your long-term goals, too.

Life insurance in your 30s can help protect future plans, like funding your children’s university fees or paying down a home mortgage.

Most people choose a policy that matches their home loan term (typically around 25 years).

If you have young kids, think about how many years they’ll depend on you financially. It usually lasts until they’re between 18 and 21, so pick the cover that stretches at least until then.

Consider inflation and long-term needs

Prices go up over time—that’s inflation. As costs rise, a policy payout that sounds good today might feel small 20 or 30 years from now.

For example, a home worth £250,000 today could easily cost double that in just two decades.

You could take out term life insurance at age 33 and ask your provider about “indexation”. That means the cover rises slightly every year to match UK inflation rates like CPI (Consumer Prices Index).

Whole of life insurance can also be useful if you’re thinking ahead to funeral costs or inheritance tax bills later on; these expenses usually increase significantly with time, too.

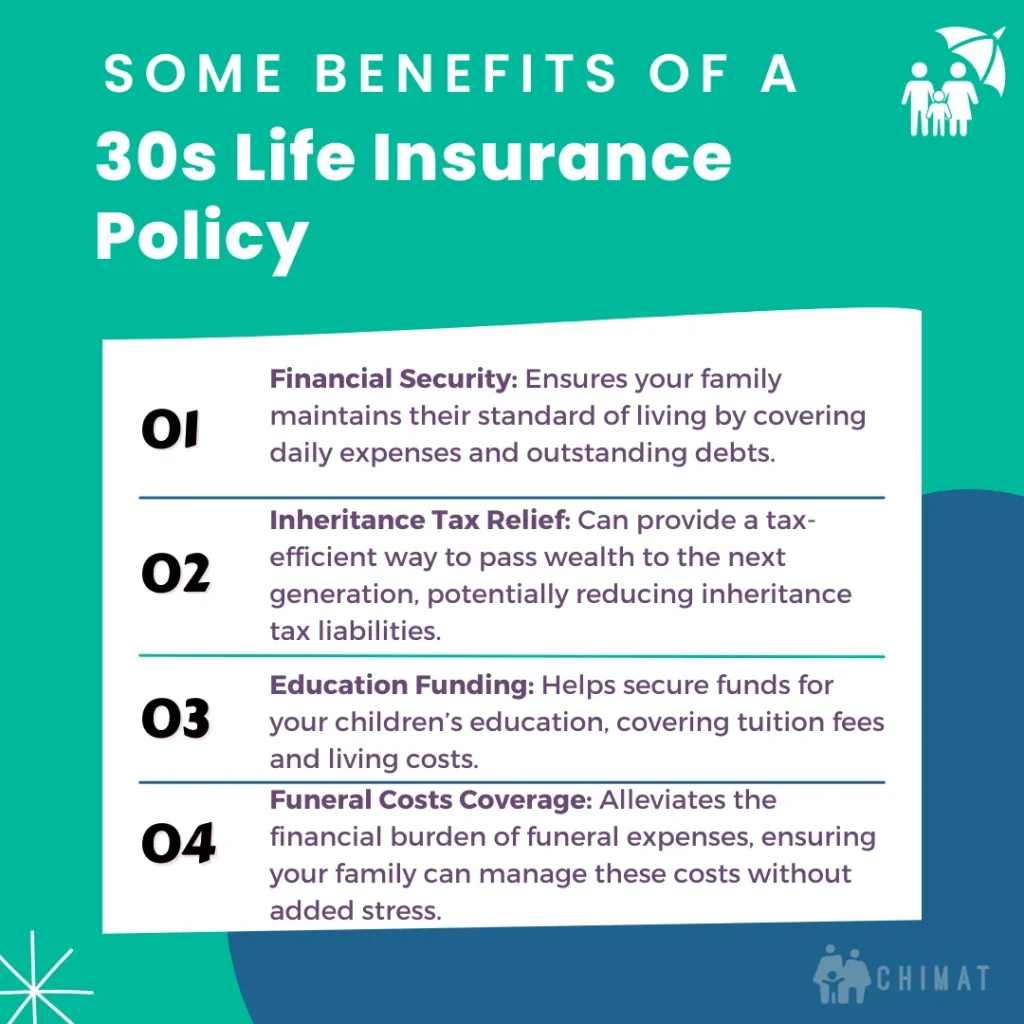

Benefits of Taking Out Life Insurance in Your 30s

It’s an age-old question: When is the most suitable time to buy life insurance? Getting life insurance now sets you up nicely for the future—it’s cheaper than waiting. You’re giving your family security early, at a price that’s easy on your wallet.

Affordable premiums

You could take out life insurance at 32 and be surprised at the low premiums are. Buying early lets you lock in lower rates because insurers view younger people as lower risk.

For example, a healthy non-smoker aged 30 might pay around £10 per month for £200,000 cover; waiting just five years can push those monthly payments higher to around £15 or more.

Life insurance companies in the UK look closely at your age and health. Younger adults often get better deals that stay fixed through the policy term.

Securing affordable premiums now in your 30s means saving money over time while still protecting your family if something unexpected happens.

Peace of mind for dependents

Life insurance gave me peace of mind for my dependents. I have two young children who rely on my income every month. Taking out a life insurance policy means they will receive financial help if something happens to me.

I feel secure knowing that mortgage bills, school fees or daily costs would be covered, no matter what.

Having life cover eases worry about family finances. My partner wouldn’t face extra stress in tough times, with funds ready to support the household needs.

Knowing this has lifted a huge weight off my shoulders and let us focus fully on enjoying our lives today.

Coverage for critical illness

Having life insurance isn’t just about securing your family’s future if you pass away—it can also protect you while you’re alive.

Critical illness cover pays out a lump sum if you’re diagnosed with a serious condition, like cancer or a heart attack.

At age 35, I chose to add critical illness cover to my policy after seeing how valuable it was for a friend who faced breast cancer at just 36.

The payment helped her stay afloat financially without worrying about bills and mortgage payments during treatment.

Critical illness insurance gives essential financial help when you need it most by covering things like medical costs, debt repayments and childcare expenses.

In the UK, you often have the option of combining critical illness cover with life insurance as one plan, which provides convenience with one premium payment each month.

This combined coverage provides security against both death and severe health risks in your thirties.

Tips for Securing the Best Life Insurance Deal

There is no need to shop around, as we can help compare quotes carefully. It’s the small details that can save you money.

Compare policies and providers

You shouldn’t rush to pick the first life insurance policy you find. Policies and prices vary greatly between UK insurers, so compare them carefully online.

Using a company like Chimat is helpful as we offer free, personalised quotes from top UK insurers quickly and easily.

Finding competitive life cover doesn’t have to be confusing. We offer clear comparison tools online that show what each provider offers and at what cost.

Scan through these details side-by-side while considering factors like premium amounts and extra benefits such as critical illness cover or joint policy discounts.

Choose the right term length

The right term length matches your life stage and goals. For instance, in my early 30s, I chose a 25-year policy to cover the mortgage on our new home—it lasted until the loan ended.

But sometimes situations change; you might move house or extend your mortgage term. In that case, extending your policy helps keep family finances safe over time.

Think about what matters most—for me, that was covering my kids until they finish university. Many people in their mid-30s opt for policies lasting between 20 to 30 years, as costs stay affordable during these ages.

Always pick insurance terms long enough to protect loved ones through major life events like mortgages or education costs.

Regularly review your policy

Once you’ve chosen the best term length, keep checking that it still suits your needs.

Your financial situation in your 30s can change quickly with home ownership, young children, or career moves, so review your life insurance policy often.

You may find you have scope to reduce term or coverage to cut costs, especially as debts shrink and savings grow.

Set a reminder at least once every two years to review your cover details carefully.

A regular check ensures you’re not paying for more protection than needed, helping you save money while keeping you fully covered through each stage of your life.

Life insurance helps keep your loved ones safe financially as your life gets busier after 30.

Getting covered early secures cheaper rates—saving you and your family money in the long run.

With proper coverage, mortgage payments, childcare fees, and daily bills can become manageable instead of stressful.

Check different providers to find the right policy at a cost that fits easily into your monthly budget.

Act now to provide security for tomorrow, ensuring peace of mind along life’s journey.

Related Questions

1. Why is life insurance important once you’re over 30?

Life insurance becomes more important after you turn 30, as your financial duties often grow—like mortgages, family costs and loans. A good policy gives peace of mind, knowing loved ones won’t struggle if something happens to you.

2. Does the cost of life insurance rise sharply after age 30?

Not always sharply—but premiums do tend to increase gradually with age. Getting cover soon after turning 30 usually means lower monthly payments and better value overall.

3. Can I still find affordable life insurance policies in my mid or late-thirties?

Yes, definitely. You can still find affordable life insurance after 30 options at this stage. Providers offer various plans tailored for people aged over 30; comparing quotes carefully helps secure a fair deal that fits your budget.

4. What type of life insurance best suits someone above 30?

It depends on personal needs. Term life policies are popular among those over thirty because they’re clear-cut and cost-effective for covering debts or supporting dependents during key years.

Whole-of-life cover offers lasting protection but tends to be pricier, so consider your goals carefully before choosing one type or another.

Research sources

- https://www.moneyhelper.org.uk/en/everyday-money/insurance/what-is-life-insurance

- https://www.gov.uk/government/publications/making-finance-decisions-for-young-people-parent-and-carer-toolkit

- https://www.onefamily.com/savings/how-to-make-a-financial-plan-for-your-family/

Paul has over 12 years of life insurance expertise. Renowned for his dedication and approachable nature, he’s a trusted advisor committed to helping clients secure their future.